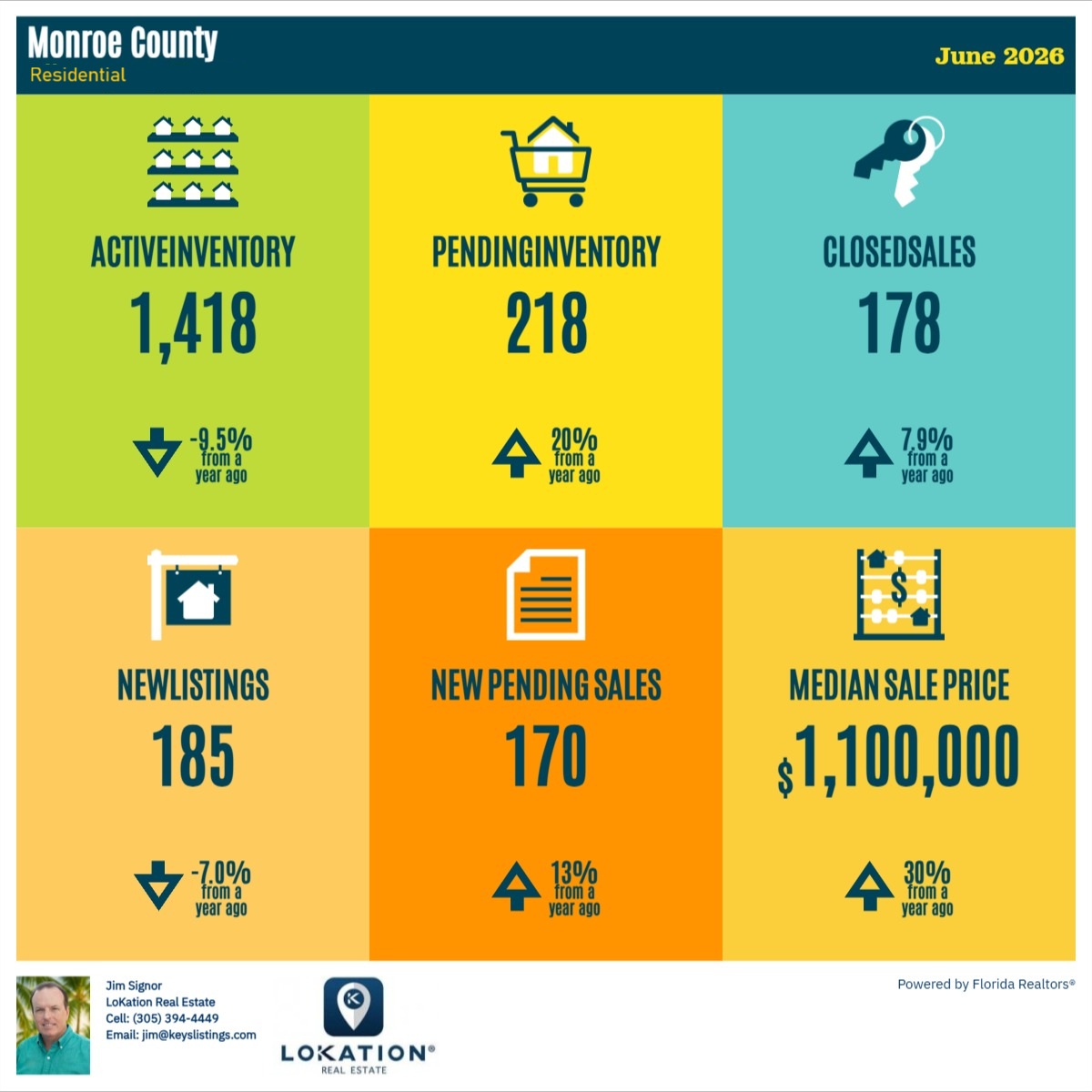

May's price acceleration was not a one-month blip. June pushed it further: compared to June 2025, the median sale price climbed 30% to $1,100,000 in June 2026, easily the strongest year-over-year gain of 2026, and it happened while both active inventory and new listings shrank.

June 2026 Key Takeaway: Florida Keys home prices climbed to a $1,100,000 median in June 2026, a 30% increase over June 2025 and the sharpest year-over-year gain of the year. The jump coincided with a shrinking supply of homes — active listings down 9.5%, new listings down 7% — while pending sales rose 13%, pointing to continued price pressure favoring sellers.

Florida Keys Residential Market Report: June 2026 vs. June 2025

The number that stands out is not just the 30% price jump, it is what happened around it. From June 2025 to June 2026, active inventory dropped 9.5% and new listings fell 7%, so supply contracted on both sides at the same time demand kept climbing. Pending inventory rose 20%, new pending sales rose 13%, and closed sales were up 7.9% over the same period.

This is the absorption story from the past few months compounding. Supply is not just failing to keep pace with demand anymore, it is actively shrinking.

Key Market Highlights — Florida Keys Residential Market, June 2026 vs. June 2025

| Metric | June 2026 | YoY Change vs. June 2025 |

|---|---|---|

| Active Inventory | 1,418 | ▼ -9.5% |

| Pending Inventory | 218 | ▲ +20.0% |

| Closed Sales | 178 | ▲ +7.9% |

| New Listings | 185 | ▼ -7.0% |

| New Pending Sales | 170 | ▲ +13.0% |

| Median Sale Price | $1,100,000 | ▲ +30.0% |

Why Are Florida Keys Home Prices Rising in Summer 2026?

Last month I called May the point where a backlog of contract activity started catching price up to demand. In my view, June shows that was not a peak, it was a pivot. Sellers pulled back too, with new listings down 7% year-over-year, which means the supply side is now working against buyers instead of just failing to help them.

In my experience, a market rarely posts its largest price gain of the year and then cools the next month. Pending inventory up 20% from June 2025 and new pending sales up 13% both point to more closings ahead, and with active inventory already down 9.5% year-over-year, there is little cushion to absorb that demand without price climbing further.

A Word to Buyers

The gap between what buyers hoped for and what the market is delivering just widened. Six months ago the conversation was about softening prices. Now the median price is up 30% from June 2025 to June 2026, and there are fewer homes to choose from than there were a year ago.

If you are waiting on mortgage rates to ease before buying, keep in mind that a large pool of buyers is doing the same thing, and shrinking inventory means that pool is competing for a smaller pie every month this trend continues. Cash buyers are not shielded from this either. There is no rate reason to wait, and the numbers say waiting has cost buyers real money every month since spring.

With new listings down and pending inventory up compared to a year ago, the imbalance driving this price growth shows no sign of easing. Browse current Key Largo homes for sale or explore Florida Keys luxury properties to see where today's median price puts you.

Florida Keys Real Estate — Frequently Asked Questions

What is the Florida Keys real estate market doing in June 2026?

It just posted its strongest price growth of the year. Compared to June 2025, the median sale price jumped 30% to $1,100,000, closed sales were up 7.9%, and new pending sales rose 13%. Active inventory fell 9.5% and new listings dropped 7% over the same period, so supply is shrinking as demand grows.

Is inventory increasing in the Florida Keys?

No. Active inventory came in at 1,418 in June 2026, down 9.5% from June 2025. New listings also fell, down 7% to 185 over the same period, meaning both current supply and the pipeline replenishing it contracted at the same time.

What is the median sale price in the Florida Keys?

The median sale price for residential properties was $1,100,000 in June 2026, up 30% from June 2025. That is the largest year-over-year gain recorded in 2026, well ahead of the 12% gain seen in May.

Is it a good time to buy a home in the Florida Keys?

In my view, waiting is the bigger risk right now. Active inventory and new listings both fell from June 2025 to June 2026 while prices accelerated, a pattern that tends to build momentum rather than reverse mid-season. Jim Signor - Florida Keys Real Estate has tracked this market since 1988, and buyers who move while quality options still exist tend to fare better than those waiting for a pullback the data simply doesn't support.

Active Key Largo listings featured on KeysListings.com. Serious buyers often begin their search here.

Active Key Largo listings featured on KeysListings.com. Serious buyers often begin their search here.